The Rapid and Epic Demise of Silicon Valley Bank (SVB)

How a bank works, what's a bank run, what went wrong with SVB and my thoughts and predictions

We just had the second-largest bank failure in US history in Silicon Valley Bank, “SVB”. (first being Washington Mutual). This week I will explain how banks work, what is a bank run, and then what went wrong with SVB, and my thoughts.

WATCH this article below:

Bank 101: How does a bank create value?

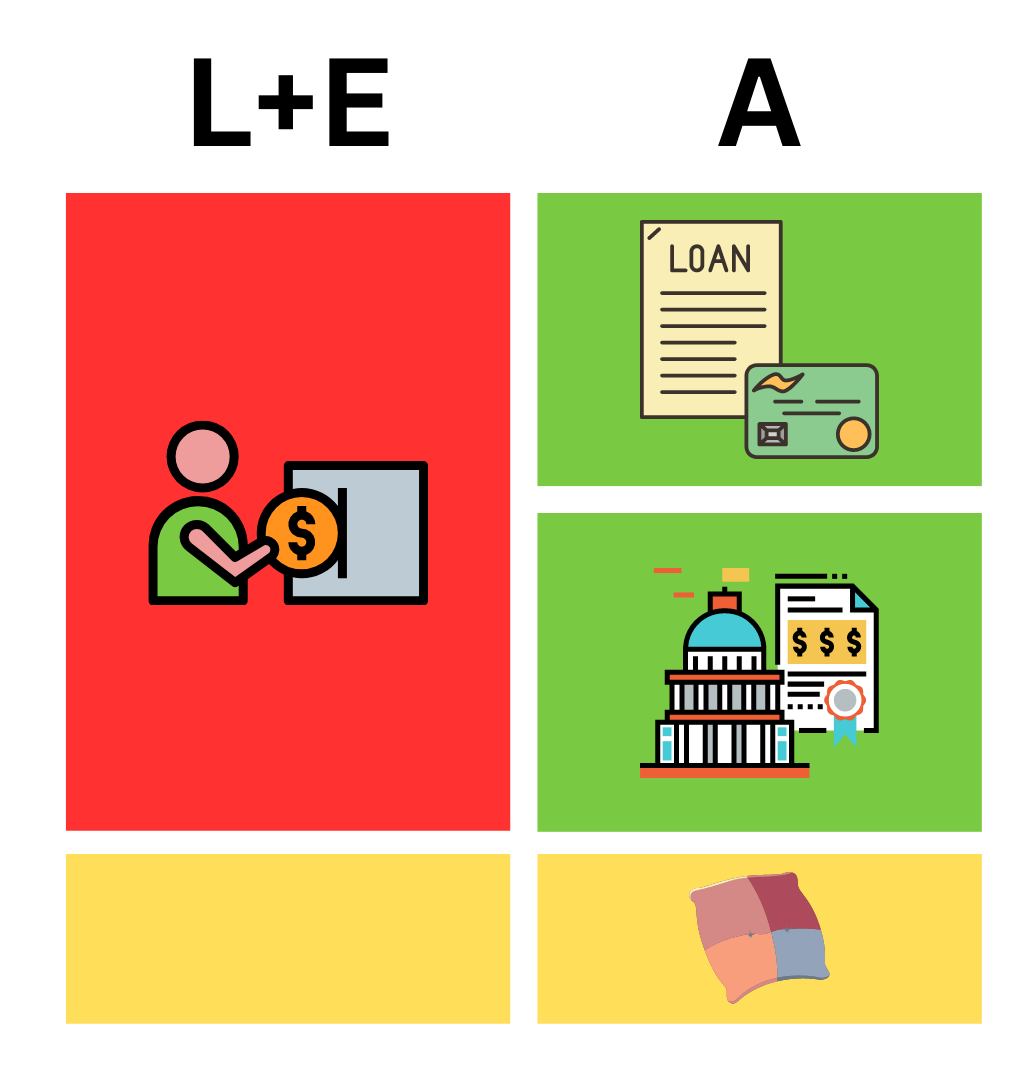

Banks are in the business of making a spread – borrow money from customers and then lend them out or invest in securities to earn higher interest than what they pay the customers.

Banks also make fees on services – minimum balance fees, overdraft fees, all sorts of fees.

This is a super simple bank balance sheet: The deposits are the sources of funding for the bank. The assets are the uses of funding such as making a loan or buying securities. By regulation, banks are required to have an equity cushion to be prepared to absorb losses on loans and investments.

If a bank does this well, the interest earned should be higher than the interest paid to depositors. The difference is called net interest income and that adds to the bank’s equity.

As you can see, asset/liability management is a crucial part of running a bank and a financial institution in general such as an insurance company.

What are the two big risks banks take on?

Credit risk

Credit risk occurs when the borrower cannot pay back the loan (and service the interest)

Lehman Brothers went bankrupt because of credit risk associated with holding large positions in subprime mortgages. And Lehman was heavily levered, it had assets of nearly $680 billion supported by $22.5 billion of equity. A 3-4% percent decline in the asset will wipe out all equity, which is exactly what transpired.

Interest rate risk

Interest rate risk occurs when the asset value declines due to interest rate increases. The longer the weighted maturity of a bank’s asset portfolio, the bigger the interest rate risk.

The S&L crisis of the 1980s was a case of interest rate risk mismanagement. A savings and loans association takes deposits and makes consumer loans (car loan, mortgage, etc.)

In 1979, the Federal funds rate was around 11.2%. To tame inflation, the then Fed chairman Paul Volcker (who proposed the Volcker Rule that prohibited banks from engaging in prop trading) raised to a peak of 20% in 1981. However, before the rate hike, many S&Ls already had done a lot of long-term loans at fixed lower interest rates. The loans devalued dramatically as a result of the interest rate increase.

To cover the asset shortfall, S&Ls needed to raise more deposits by offering higher market interest rates, but the interest on loans was grandfathered into a lower rate, so S&Ls were earning negative interest spread because of this mismatch.

Losses were piling up and reducing equity capital. The end result was nearly one-third of U.S. S&Ls failed during the period from 1986 to 1995.

What is a “bank run”?

Depositors don’t want to lose their money, so when there is a PERCEPTION that the bank might fail, depositors will panic and withdraw money at the same time. That’s called a bank run.

The key word is PERCEPTION. There are things a bank can do to fix the issue, but FEAR and PERCEPTION can trigger the actual downfall of banks, which is what happened in SVB’s case.

What went wrong with SVB?

On March 8 after-market, SVB put out a press release stating it incurred a $1.8 billion after-tax loss after selling its $21 billion available-for-sale portfolio and is raising external capital. SIVB stock lost 60% of its market value the next day. Depositors panicked and requested to withdraw $42 billion the next day.

Two days later on Friday, March 10, SVB was deemed insolvent and put into FDIC receivership.

What went wrong? It’s really a combination of mismanagement of the asset side and a bank run from a unique depositor base on the liability side.

On the asset side, SVB bought a sizeable amount of long-term treasury bonds with ~2% interest, which is very poorly positioned against a rising interest rate. It’s poor interest rate risk management.

Coming out of the pandemic, the government pumped a lot of money into the market, resulting in a lot of deposit inflow into the banks. Banks needed to create value with those deposits. Otherwise, they make negative spreads. There were three camps of thoughts on what to do with the surge in deposit money:

Staying in cash

Tactically trading short-term bonds. JP Morgan went with this approach.

Buying longer-term securities for the yield. SIVB went with the third option and they weren’t the only one.

You might wonder: “Why didn’t SVB make loans instead of buying long-term treasury?” Well, the supply of money was growing more quickly than the demand for loans, so banks had no option but to either stay in cash or park it in securities to earn some income.

It’s not a crime to earn some 2% income, especially when the shorter-term bonds were offering even less income. However, locking in trough interest rates in long-duration securities exposed these securities to an interest rate upswing. And then inflation surged, and The Fed raised interest rates. Now the market interest rate has more than doubled to 4.5%.

You know what they say, can’t lose money unless you sell right? When banks buy securities, they can decide to designate them as held to maturity (HTM) or available for sale assets (AFS), which have different accounting treatments.

AFS are marked to market. On the other hand, if the securities are designated as HTM, the pro is it’s not marked to market. The con is when a bank decides to sell even a single security in an HTM portfolio, the entire portfolio will be marked to market and trigger a big hit to the firm’s equity capital.

When interest rate was low and stable, many banks favored the flexibility of AFS designation to be able to buy and sell bonds without seeing much fluctuation in bond values.

Now the interest rate started rising, many banks reclassified AFS securities as HTM, which will protect the financial statements from further “losses”.

But AFS or HTM, the reality is if banks owned long-term securities, unrealized losses started to pile up and it’s just a matter of time before the world knows they are swimming naked. According to the best Substack writer for Financials sector1, SVB’s equity was technically insolvent in September 2022 if its HTM portfolio were to be market to market.

Meanwhile, on the other side of the balance sheet. A rising interest rate means higher borrowing costs for start-ups and slowing demand for the customers of these start-ups, and they started withdrawing money from SVB to meet cash needs.

When depositors withdraw money, the bank needs to sell securities on their book to raise cash to honor the withdrawal because most banks only hold a fraction of their deposits in liquid assets. This is called “fractional reserve banking”, which is the system used in banks in most parts of the world.

The problem is SVB cannot raise money by selling a single bond in the HTM portfolio without triggering a mark-to-market and the bank did not have sufficient capital to absorb the loss. So they had to resort to external financing and selling their smaller AFS portfolio, which resulted in the March 8 press release. But that press release created more fear in its customers, which drove more withdrawals.

Unlike a typical commercial bank, SVB has a concentrated depositor base:

For example, Chase bank has 66 million households as depositors. And these 66 million households are unlikely to know each other and hang out in the same Twitter space or Clubhouse chat rooms. Well, I could be wrong, never say never? For Chase bank to face a credible bank run, a large number of small depositors need to act in unison to move the needle as each customer is unlikely to be a material portion of Chase’s overall deposit base.

In contrast, SVB has only 38k customers. They are not mom-and-pop depositors. Most of SVB’s depositors are start-up companies and venture capital firms. For SVB, a small number of customers can constitute a majority of SVB’s total deposits. According to regulatory filings, about 90% of SVB’s deposits are not FDIC insured as a lot of them probably have millions of cash deposited with SVB.

And SVB’s customers, the start-ups and the VC firms, are talking to each other offline and online on Twitter. When one was withdrawing money, so were the others. Putting the nail on the coffin, they are advised by the same set of venture capital firms, whom they rely on for both financing needs and strategic guidance. If someone as credible as Peter Thiel told all his fund’s companies to pull money out of SVB, the start-ups will take the advice and act in unison, which can drain the bank’s deposit base rapidly.

And the dominos started falling quickly as SVB was losing deposits in chunks. Ultimately the external financing never got done so SVB couldn’t come up with the cash to honor the withdrawals.

On Friday, March 10, state regulators took possession of the bank and placed it under the receivership of FDIC. And a Deposit Insurance National Bank of Santa Clara was created.

The Aftermath

Initially, depositors were promised access to only an FDIC-insured portion of their money at the newly formed Deposit Insurance National Bank of Santa Clara. Over the weekend, the Treasury Department, the Federal Reserve, and FDIC jointly announced that SVB depositors will have access to all of their money starting Monday, March 13 and no loss will be borne by the taxpayer. Instead. the Deposit Insurance Fund, which comprises the FDIC insurance premium all the member banks pay, will be used to make depositors whole.

SVB has a new CEO. SVB employees will have 45 days of employment and are offered 1.5 times their salary to stay. That makes sense given the current employees have invaluable system knowledge of how the bank operates.

The press dug up that prior CEO Greg Becker sold $3.6 million of company stock on February 27, 2023, just a week before the press release. And the bank paid bonuses to employees literally hours before the government takeover.

The bank sector stocks have sold off. Investors are rightfully concerned that some regional banks’ asset portfolio is similarly positioned as SVB’s and could face solvency issue.

There were chatters that some start-ups were going to lay off people on that Friday but couldn’t because they didn’t have the cash to pay severance.

Many VC firms publicly announced support and pledged to continue the business relationship with SVB.

My Takes and Predictions

What will happen to the research franchises, Leerink and MoffettNathanson? I think they will be fine, they have a reputation in their respective sectors. Leerink for healthcare. MoffettNathanson for TMT and payment. Craig, Mike, Lisa, and Sterling are all top-notch analysts. They will probably be sold because SVB’s ambition of becoming a force in investment banking is now over.

Crises will happen again. Because we human beings are greedy and foolish. It will just come in different forms. In 2008, it was real estate, MBS, CDO, CDO2, was there CDO3? During the pandemic, it was crypto, WallStreetBets, metaverse real estate, NFT. Now we are finding out who is swimming naked in the banking sector when the tide of free money goes away.

I can’t speak for anyone else, but Howard Marks would not have made the mistake of not knowing where we are in the cycle. If you haven’t read his newer book Mastering the Market Cycle, I highly recommend it. When rates were at 1.8%, it’s very asymmetric how much rates can go up than go down. Why would you invest a big portion of client money into long-duration securities that are exposed to this risk? I start to see why Jamie Dimon is paid the big bucks because that guy just gets it and does his job. Whether these regional bank executives are just greedy with their eyes closed and hoping for the best or they are just wrong, I don’t know.

As trust in the regional banks erodes. The big four, JPM, Wells Fargo, Citi, and BofA are seeing massive deposit inflow. But I am highly confident the too-big-to-fail banks will do something stupid again in the future to remind everyone that no bank is truly safe.

The timing of the SVB’s press release was very poor because the crypto bank Silvergate Bank announced the wind-down of operation on the exact same day. Trying to raise financing right at the same time as another bank’s failure is not perceived well. But I guess how the heck do you coordinate these news flows?

There is definitely animosity toward VC firms “pulling the rug” by telling their portfolio companies to withdraw money. The most publicized one was Peter Thiel, who is the author of Zero to One, a great book. His own VC fund withdrew all the money from SVB before the blow-up and he advised all his companies to do the same. I will pull a sell-side research analyst here with a neutral view: On one hand, I don’t think it’s wrong to protect your own firm and your portfolio companies by telling them to preserve access to liquidity, which is the lifeline for start-up companies. On the other hand, I am sure some VC firms have the motive of seeing SVB fail because they financed neo banks who can eat into SVB’s market.

Social media became an accomplice of something again, this time a bank run. And it just shows in an increasingly interconnected world, how much more quickly things could happen than in the analog world. Just something to keep in mind.

Moral hazard is always a topic during times like these. Despite no taxpayer needed to bail out the depositors, the insurance premium money to make depositors whole is kind of like SVB freeriding on the other FDIC bank members who didn’t f**k up their portfolio but have to pay for SVB’s mis-execution. Is it right for others to pay for your failure? No, BUT even the traditional insurance model is based on the good actors subsidizing the bad ones, or the fortunate subsidizing the unfortunate.

And the government had to think very big picture about the implication of SVB’s failure. In this case, do you want the start-up community to lose faith in the banking system? And without a start-up ecosystem, could we, the United States, lose our edge for incubating innovation to another country? That’s probably the reason over the weekend the government reached the conclusion of making SVB depositors whole because of the risk it can pose to the entire system.

In my view, this whole SVB fiasco could have gone very differently if SVB went out to raise private financing to shore up the equity, they might be just fine. It’s quite unfortunate how it transpired, but I think the VC ecosystem’s endorsement of the bank means there is still some trust there.

Thanks for reading. I will talk to you next time.

If you want to reach 3,000+ equity investors, contact me 👇

Check out my other published articles and resources:

📇 Connect with me: Instagram | Twitter | YouTube | LinkedIn

If you enjoyed this article, please subscribe and share it with your friends/colleagues. Sharing is what helps us grow! Thank you.