How do you generate variant views?

A case study

To make money in stocks, you need to believe in a different outcome for a business that the market is not pricing in, AND more importantly, you need to be right.

That's why investing is harder than many newcomers think: It’s NOT about buying the lowest valuation stocks or buying the best or fastest-growing business at any valuation.

I have been burned in the former scenario plenty of times, and I am sure some of you have learned the lesson the hard way in the latter scenario during the 2020-2022 period. Exhibit A below.

How do you generate the correct and variant views? Here comes the bad news: THERE IS NO SHORTCUT. You need deep expertise in the industry you are looking at and a broad range of pattern recognitions so that, hopefully, some of the mental models help you understand the situation at hand.

Today, I will walk you through an investment case shared by the famed value investor Li Lu of Himalaya Capital on a misunderstood South Korean IPO.

The research job board is here! Fast-track your job search process so you can focus on perfecting your stock pitches and networking. All U.S. buy-side and sell-side equity research job leads are in one place.

Megastudy

Megastudy (KOSDAQ: 072870) is a South Korean1 tutoring company that prepares high school students for the most crucial exam of their lives - the college entrance exam, or the Suneung (수능.)

In Korea, as well as many other parts of Asia, the college one attends significantly influences the caliber of companies one can work for throughout their career. (“target school” is a similar concept but more industry-specific)

Many individuals in these regions work for a single company their entire lives, such as working for Sony or Samsung. As a result, students and parents are deeply invested in exam preparation. The emphasis on exam scores by college admission offices creates a high demand for after-school tutors. This demand, coupled with the limited availability of good tutors and their time, results in pricing power for the best tutors.

Megastudy, as a first mover, capitalized on this market dynamic. By hiring top teachers, recording their tutoring sessions, and making the content available online, the company made the best test preparation content affordable for a broader audience, not just the affluent, while creating a more scalable business model.

Megastudy was readying for its IPO in December 2004 after growing revenue by triple digits while achieving a 40% operating margin in the prior 3 years.

The IPO was priced at 18,500 won. For a business with 6.3 million outstanding shares and 50 billion won in cash post-IPO, assuming a 1:1000 USD:KRW exchange rate, this translated to a ~$120 million market cap for a business that did $15 million in earnings in 2003 (net profit in the exhibit above,) which is 8x 2003 earnings for a monstrous ROE business. Assuming continued revenue growth in 2004, it’s even cheaper on 2004 earnings.

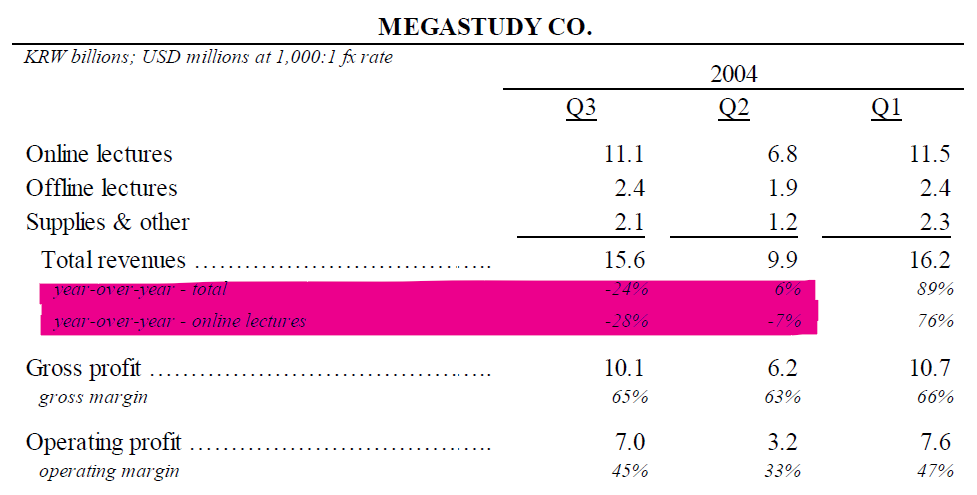

Why was Megastudy so cheap at IPO? Well, in April 2004, the Korean government released a free tutor service that is perceived to be a competitor to Megastudy. What happened to Megastudy’s business after the launch of the government service?

In the second quarter of 2004, Megastudy's online lecture revenue fell by 7% y/y. In the third quarter of 2004, online lecture revenue dropped 28% y/y. Now, perhaps a business facing an existential threat from a government-sponsored alternative deserves an 8x 2003 EPS valuation.

Was Mr. Market right? Or was this a big opportunity to buy a deeply discounted market leader that provides a mission-critical product to Korean high school students? How do you generate a variant view?

First, let’s understand the government’s new product: the government pays its teachers a fixed salary, while Megastudy gives its teachers a 23% commission on all the lecture fees they generate.

As Charlie Munger famously said: "Show me the incentive, and I will show you the outcome." Top teachers are likely to stay with Megastudy because of the 23% revenue share, while mediocre teachers may work for the government’s service, knowing they have limited ability to attract a sizable fan base. In fact, the fixed salary provides a nice downside protection.

On the customer side, what do students and their parents value the most? Price or getting the best product to maximize their chance of attending top schools like Seoul National University? They value the best product. Megastudy, with the best teachers, will attract customers with the willingness to pay.

What’s the barrier to entry for tutoring services? What if a new entrant offers a 33% commission to attract the best teachers?

Back to the incentives. Ultimately, teachers care about the absolute dollar amount they can take home. Megastudy, being the scale player, has the highest absolute dollar amount of the fee pool, making the 23% commission more attractive than 33% of a fee base with a new entrant that is 1/10 of Megastudy’s. (eg. 23% of $100,000, or $23,000, is more attractive than 33% of $10,000, or $3,300) Therefore, Megastudy will likely attract the best teachers because they have the most students (and fees.)

The two sides form the flywheel: the more students use Megastudy, the more dollar commission tutors can earn. Knowing the commission prospect, the best teachers will flock to Megastudy, which attracts more students.

How should Megastudy solidify its position? Very simplistically, help students score high on the Suneung. That’s it: drive results and customers will come.

Megastudy’s founder was one of the exam teachers in the country and he had connections with all the top teachers in different subjects, to whom he offered equity to. As the first mover, Megastudy was able to achieve initial critical mass with all the top teachers.

In Hamilton Helmer’s 7 Power framework, Megastudy enjoys access to cornered resources (top teachers), and builds scale benefits and network effects over time which also translates to a brand. Meanwhile, the government’s free service is expected to be left with mediocre teachers.

We conclude that the government’s free service is no threat to Megastudy’s positioning, and Megastudy will likely be the long-term winner in the Korean tutoring market. We will invest in the company at 8x 2003 EPS.

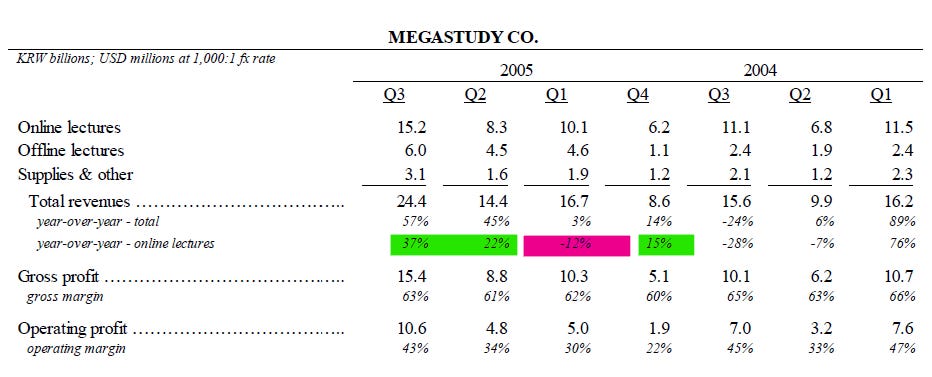

What happened in the fourth quarter of 2004? Online revenue increased by 15% y/y. Maybe we are right; Megastudy isn’t affected. Or perhaps Megastudy is dressing up the results to help sell the IPO. Both are possible.

Heading into 2005, what happened in 1Q? Online revenue was down 12% y/y, top revenue was up 3%. The college entrance exam takes place in November of each year. Maybe students are trying the government's new service because there is a lot of time left. If they find out the government product is subpar, and they can commit to Megastudy.

If you haven’t done the work and come to the conclusion above, maybe you say, "Okay, Megastudy is losing market share." Or this was the time to double down and buy the stock (Note: Li Lu bought more) because you believe the government service is not a competitive product (easy to say after the fact, of course).

What happened in 2Q of 2005? Online revenue increased by 22% y/y, and total revenue went up by 45% y/y. This quarter was crucial, as students became more serious about preparing for the exam, which takes place less than half a year away (November.) Perhaps now the students have tried the government product and are now flocking to the market-leading product.

What happened in 3Q of 2005? Online revenue was up by 37% y/y, and total revenue grew 57% y/y. The reacceleration likely came with the multiple expansion that moved the stock upward.

Final question: will Megastudy dominate the online tutoring market? In hindsight, it did. Megastudy overcame the threat of new entrants (which distills down to the flywheel of having the best product that attracts the most customers) and the government’s free service. Revenue grew by 50% annually in the next 3 years while maintaining a 35% operating margin, boasting revenue six times larger than its closest competitor. The stock became a 10-bagger.

What did the market miss? It incorrectly perceived the government’s free service to be an existential threat to Megastudy’s business model.

As you can see, the variant view involves using reasoning and fundamental analysis frameworks to gain conviction. I hope this proves to you that there is no shortcut to outperforming in the stock market – it requires hard work, pattern recognition, courage, and temperament. All of these are easier said than done, and most fail at the hard work part.

Epilogue: Li Lu pointed out that by the time the stock had 10-bagged, Megastudy traded at 30x earnings and had a 80% market share in online tutoring services. Was the stock still a buy then? In hindsight, based on the stock chart (basically flat for a decade), NO. I don’t know what ensued, but it’s safe to assume they struggled to come up with new ways to grow. However, this is beyond the scope of a wildly successful multi-bagger investment over just three years. If any of you know what happened to Megastudy after 2007, please tell me (just curious)!

Thanks for reading. I will talk to you next time.

If you want to advertise on my newsletter, contact me 👇

Resources for your public equity job search:

Research process and financial modeling (10% off using my code in link)

Check out my other published articles and resources:

📇 Connect with me: Instagram | Twitter | YouTube | LinkedIn

If you enjoyed this article, please subscribe and share it with your friends/colleagues. Sharing is what helps us grow! Thank you.

Reference:

https://www.scribd.com/document/579106890/Li-Lu-Lecture-2012

Future mentions of “Korea” in this article refer to South Korea

Nice write-up with a clear divergence between the market & variant views. In this case, did Li Lu identify a clear catalyst that could correct the market's (incorrect) view to match his own? Or did he make the investment under the idea that the market would gradually converge as the company reported results over time? Curious about when it is appropriate to identify a catalyst as part of a thesis vs. trust that the market will gradually get it right

No asymmetry between perception and reality, no outsized returns.

Great post!