Bill Gurley Talks Publicly Traded Internet Companies

Learning from one of the greatest venture capitalists

I have consumed a lot of Bill Gurley's content over the years, and he is arguably one of the best thinkers on network-based businesses.

To my early followers (who knew me as the most dominant social media person in the ultra-niche space of sell-side equity research), Bill Gurley used to be "one of us": he was once a sell-side equity research analyst at Credit Suisse First Boston during the era when Frank Quattrone was making it rain as the king of tech IPOs. At the age of 24, Gurley became a lead analyst and covered companies such as Dell, Compaq, and Microsoft, and was the lead analyst on Amazon.com's IPO.

In 1996, Frank Quattrone called him and said he is leaving Morgan Stanley and he has heard good things about Gurley. Quattrone wanted Gurley to come with him to Silicon Valley. Gurley met him after figuring out how important Quattrone is (he is very important even to this day as a legendary investment banker). Gurley told Quattrone that he doesn’t want to do sell-side research for much longer and voiced his aspiration for VC. Quattrone persuaded Gurley to move with him in exchange for introducing Gurley to every VC he knows.

The rest is history - Gurley went on to become one of the prominent venture capitalists. Today he is a billionaire and a general partner at Benchmark Capital. Some of the high-profile companies he invested in include GrubHub, Stitch Fix, Zillow, and OpenTable.

Interesting fact: Gurley stands at 6'9" and played college basketball for the University of Florida Gators.

My discussion is based on an early podcast episode between Gurley and Patrick O. on my favorite podcast show, Invest Like the Best. If you're interested in listening to the entire podcast, click on the link below:

Network Effect

The beginning is always hard, and that’s true for business building. However, for some companies, once they reach a certain size, they find it even easier to get to the next level. I remember one motivational speaker used the line “The first million is the most difficult, and the second million is inevitable”. Having reached very minor success across many social media platforms, I find that to be very true.

Gurley used Microsoft as an example: as more people wrote apps for Windows, the value of the platform increased, making more people want to write apps for Windows, creating a virtuous cycle. Once the flywheel is in motion, it's hard to stop.

Many start-ups claim to have a network effect in their pitch deck. The phrase is often overused. You, as the investor, need to use your judgment to decide whether a business truly has a network effect and determine the strength of it.

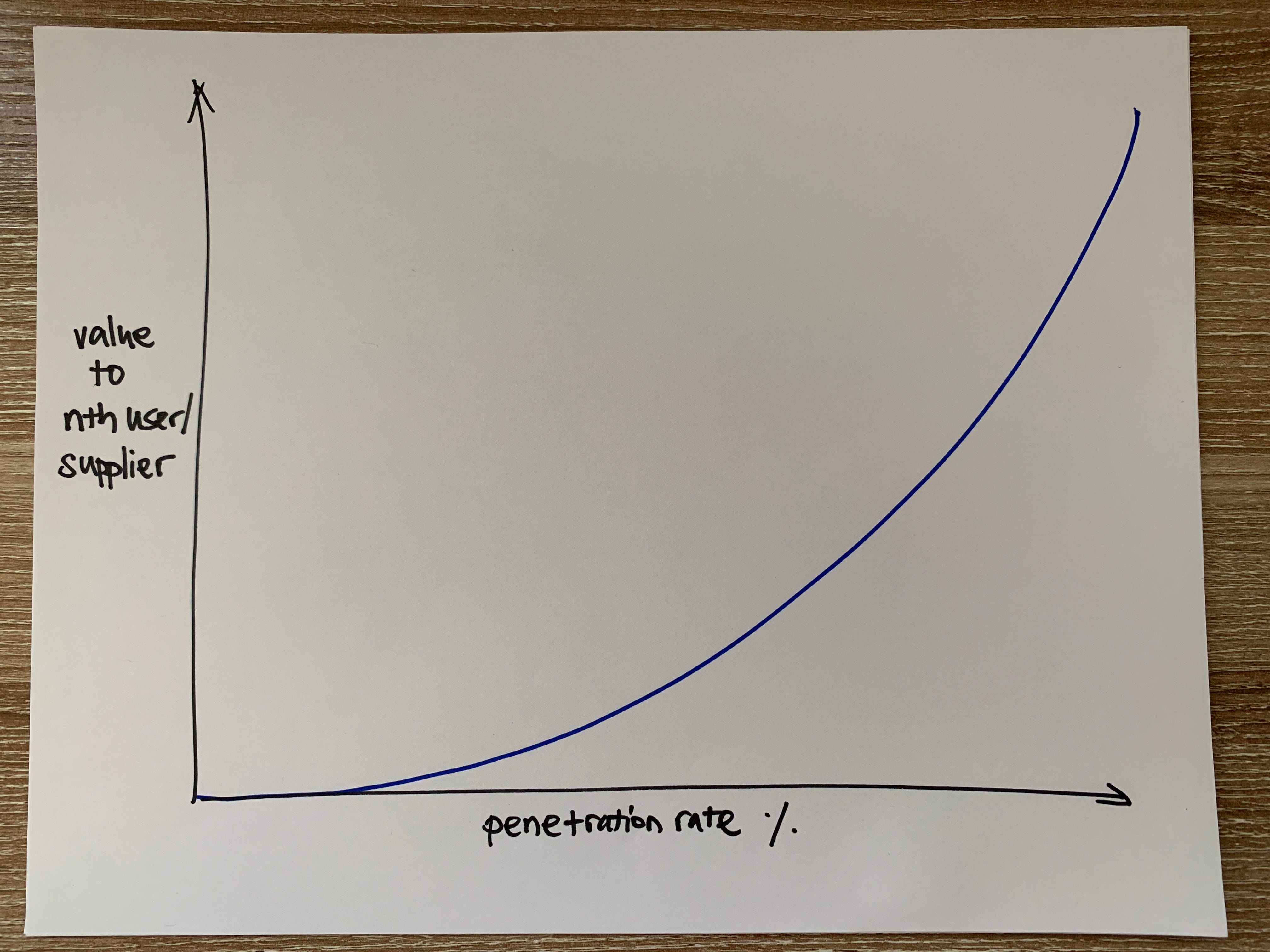

To assess whether a business exhibits a network effect, Gurley has an unpublicized rule of thumb: Imagine an X-Y graph, with the Y-axis representing the value to the customer and the X-axis representing the penetration into the market. If it's a two-sided network, do one graph for the supplier and another one for the consumer. Is the line between the two things going up and to the right? If yes, there is a network effect.

For UGC-based (user-generated content) platforms, the opportunity is incredible once you can tip over into the flywheel (eg. Pinterest, Twitter, Instagram, Nextdoor) Gurley’s Pro Tip: do un-scalable things to get the network effect going. Here are examples of how public internet companies solved the cold-start problem:

Yelp: Founder Jeremy Stoppelman would go to SF nightclubs to get Yelpers excited about the platform. There is no way Jeremy could visit every business listed on Yelp, so he focused on engaging passionate party-goers who cared about the quality of reviews and the frequency of reviews was high. Once the flywheel started working in one geographic area, Yelp replicated the same playbook. This approach proved better than attempting to scale nationally or globally without first achieving critical mass in a hyperlocal network. Yelp's competitors, Judy’s Book and Insider Pages, who had more VC financing, made the mistake of focusing on breadth instead of quality: they allowed anyone to review any business.

Glassdoor: Cisco became the first company to be reviewed on Glassdoor. The founders of Glassdoor went to a Starbucks near Cisco with a pad of paper and interviewed Cisco employees for reviews.

Tinder: Tinder threw parties in each city they launched to attract quality daters and raise the overall experience level.

Nextdoor: Nextdoor didn't open up a neighborhood to users until the neighborhood had at least 10 members. This prevented a “ghost town” experience, as the quality of the network business experience depended on how many neighbors were actively using the system.

Because UGC businesses can grow rapidly due to their low marginal cost, Gurley advises not to focus on monetization until a critical scale is achieved. He mentioned a number like 10 million users when this podcast was recorded in 2019, but this figure may have changed since then.

Flaws of Labor Marketplaces

Building a marketplace that connects labor is tricky, although it has been achieved with platforms like Fiverr, Upwork, and Angi. Using Gurley's XY framework, the problem lies in the absence of incremental value once a marketplace aggregates more than 5% of the labor supply. In other words, the value of the marketplace does not significantly differ between owning 5% of the labor supply versus owning 95%.

This makes it difficult to achieve network effects beyond a small level of penetration in the supply base. Consequently, there is a risk of fragmentation, and another competitor can focus another 5% of the labor supply to compete, preventing a winner-takes-all scenario.

Monogamy can be detrimental to marketplace businesses due to the risk of disintermediation. When customers find good service providers like haircutters, babysitters, doctors, or dentists, they tend to stick with them for an extended period. This poses a challenge for marketplaces because: 1) the customer is no longer actively searching, and 2) the customer and service provider may take their transactions offline, bypassing the marketplace that facilitated their initial connection.

In contrast, the restaurant industry presents a better proposition because it is more prone to promiscuity. Customers tend to try new restaurants frequently, even while having their favorite ones. A well-designed platform can reduce the search costs involved in discovering new restaurants, which could explain Gurley's investment in OpenTable.

Aggregating Demand or Supply?

To Gurley, demand is the game. Most suppliers are easy to sign up. Big marketplaces were built on the value proposition of aggregating highly fragmented SMBs that have not been in business for long, helping them get discovered. For instance, Expedia aggregated small hotels and hostels that didn't have the brand recognition of Marriot or Hilton to create their websites and increase their visibility.

That's why you don't see marketplaces that aggregate supply in fairly consolidated industries. In such cases, the marketplace has no bargaining power. All industry players can go directly to consumers without relying on a third-party marketplace. For example, airlines have their websites for travelers to book flights, which is why Google Flights doesn't charge anything because airlines and travelers wouldn't pay for such a service.

Gurley cited the case of Grubhub: Grubhub’s competitors were focusing on servicing big chains like McDonald’s, Quiznos, and Subway. They all went bankrupt because they were unable to establish a strong bargaining position.

What Isn’t Network Effect?

Companies with heavy marketing spend, especially on consumer acquisition, usually aren’t marketplaces and lack network effects.

In any industry, a company can act as an outsourced marketing service provider, aggregating suppliers and purchasing media on the suppliers’ behalf when supplies lack the expertise for effective marketing. The company can generate and sell the leads to suppliers at a higher price than what they paid for the leads, earning a spread.

The market is efficient in valuing lead-generation businesses, and they typically trade at one or two times revenue because they lack network effects. For example, the auto advertising platforms like Cars.com, CarGurus, and TrueCar operate more as lead-generation businesses rather than true marketplaces with network effects.

Valuation

Most entrepreneurs think they deserve 10x revenue without considering what revenue represents. Not all revenue is equal. In the long run, only companies that allocate capital wisely and generate returns on invested capital can achieve higher valuation multiples.

At the time this podcast was recorded in 2019, private companies had more financial power and were challenging the incumbents. It’s fascinating to fast forward to today how the market regime has changed yet again. Just be very careful with the phrase “this time is different.”

On Regulatory Capture

Regulatory capture is the phenomenon where a regulatory agency ends up serving the interests of the industry it is supposed to oversee, rather than protecting the interests of the public. ChatGPT explained to me regulatory agencies can be influenced by various factors, such as:

Lobbying, often with incumbents opposing the regulations having the largest lobbying budgets

Revolving doors, where regulators move between government agencies and private practices, leading to conflicts of interest

Informational asymmetry, where regulators lack the expertise or resources to fully understand the complexities of what needs to be regulated, leading them to rely on information provided by industry experts, creating bias

Sympathy, the agency develops sympathy towards the interests of the industry they regulate.

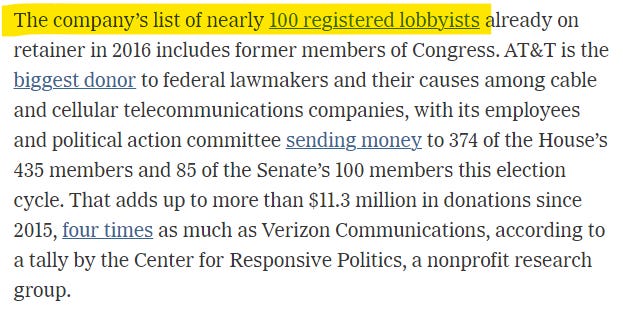

Gurley provided an example of financing a business called Tropos with the vision of providing city-wide WiFi. The company approached various towns in Texas to convince the mayors about implementing their services. However, AT&T, with lobbyists in every county in Texas, exerted its influence and eventually forced Tropos to shut down its services.

Importance of Specializing

Alright, so Gurley is not in the Munger camp. Gurley emphasizes that the availability of information empowers everyone to learn as much as possible about a subject matter where they can become experts.

Gurley advocates for becoming a historian of an industry of your interest. By studying the pioneers and understanding the history, you can establish a solid foundation of knowledge to form a prudent view of the industry's future. This perspective aligns with what Seth Klarman mentioned about being a student of financial history.

The key is to be hyper-curious. Gurley is still a voracious reader today.

How to Find a Mentor

Everyone has the will to win, but not the will to practice: Do your homework. Read everything about them. Show immense respect for them. You are luckiest when preparation meets opportunity.

Thanks for reading. I will talk to you next time.

If you want to advertise on my newsletter, contact me 👇

Resources for your public equity job search:

Research process and financial modeling (10% off using my code in link)

Check out my other published articles and resources:

📇 Connect with me: Instagram | Twitter | YouTube | LinkedIn

If you enjoyed this article, please subscribe and share it with your friends/colleagues. Sharing is what helps us grow! Thank you.

Interesting history!

🙌