Housing Market Trends with Ivy Zelman

Things are just fine, but that's not good news for home buyers

Looking to buy a home? Do you care to know where we are in the housing cycle? There is no better person to ask than Ivy Zelman. Let me share with you her pulse check on the U.S. housing market.

What you will learn about:

The current state of the U.S. housing market

Mortgage rates and spread trends

Multifamily market

Secular drivers of housing demand

And so on

Do you enjoy the Equity Analyst, you should check out the Pari Passu Newsletter!

Pari Passu's newsletter is written by a restructuring banker turned private equity investor who enjoys sharing lessons about investing (in both a public and private market context) and many other topics. Some of his great posts include: deep dive on Amazon, When to Quit book summary, Trimark USA restructuring summary.

These are some of the things readers say about Pari Passu:

“Not doing restructuring but your newsletter is one of the only ones I really look forward to reading together with Matt Levine’s money stuff”

“I am yet to go through and process quite a lot of your content, but very impressive and interesting I must admit”

“Landed an offer during on-cycle, everything I learned reading the newsletter was immensely helpful - especially the Bain PE Summary”

Ivy Zelman is the founder and CEO of Zelman and Associates, an esteemed independent equity research boutique. Zelman accurately predicted the Housing Crisis in the 2000s, which propelled her to legendary status on Wall Street. Her exceptional achievements have led her to be enshrined in the Institutional Investor Hall of Fame, with 18 appearances in total and an impressive record of being ranked No.1 ten times in her sector.

U.S housing markets

Despite the attention-grabbing headlines, the U.S. housing market has been surprisingly resilient. The number of transactions hovers around 5 million, compared to the historical rate of 6 million per year. However, the existing and new home markets tell different stories.

The existing home market is grappling with tight supply conditions, driven by:

Record-low inventory levels: one million homes available for sale versus 2 million during the peak of COVID.

Current homeowners are not motivated to move because 90% of them have locked-in mortgage rates below 5.0%, and 50% of them have mortgages below 3.5%.

An aging population has resulted in reduced mobility (Ivy cited that the population aged 18 to 24 moved around 50% of the time, whereas the 55 to 64 age group has a mobility rate of only 7-8%). This trend started in 2013 and has only accelerated, compounding tight inventory.

In contrast, the new home market is thriving, now accounting for 15-20% of total housing market transactions, compared to 10% pre-COVID. The share gain is driven by a stronger relative supply when demand remains strong. Demand has progressively shifted towards the new home market, leading to a surge in stock values for homebuilders throughout 2023.

Why hasn’t the interest rate hike cooled the housing market?

Historically, a rise in mortgage rates accompanied by increasing mortgage spreads (above the 10-year Treasury) would lead to a slowdown in the housing market. Zelman highlighted that the housing market did weaken during the Fed’s tightening cycle when rates initially increased, notably in nine months in 2022, with some markets experiencing price drops of up to 20%. However, the market has seen a positive reversal in 1H 2023 for several reasons:

Homebuilders have strategically adapted their inventory management by offering mortgage rate “buy-downs”. This approach entails the homebuilders absorbing the cost of lowering mortgage rates below the market to incentivize buyers. Homebuilders choose to compromise on their gross margins rather than contend with the financial burden of carrying high inventory along with substantial maintenance costs.

Additionally, the robust economy characterized by job growth and wage inflation has bolstered the housing market's durability.

The transfer of $80 to $100 billion of wealth from Generation X and Baby Boomers to their millennial and Generation Z offspring, via down payments and even outright home purchases, is supporting the demand.

What’s driving the higher mortgage spread?

Currently, the mortgage spread is about 300 basis points above the 10-year Treasury yield, which is impacting mortgage affordability.

This elevated spread is driven by the Federal Reserve's reduced role as an MBS (Mortgage-backed Securities) buyer, heightened demands for returns from MBS investors due to economic weakness and delinquency risks, and the potential for increased prepayment risk if rates decline significantly.

This complex interplay affects actual mortgage rates, as lenders respond to higher MBS spreads by adjusting mortgage rates to align with investor demands.

The Fed's historical influence in the MBS market, transitioning from major buyer (to lower rates and stimulate the economy) to non-seller, has played a significant role in shaping this scenario. Any decision by the Fed to resume selling MBS would exert upward pressure on rates.

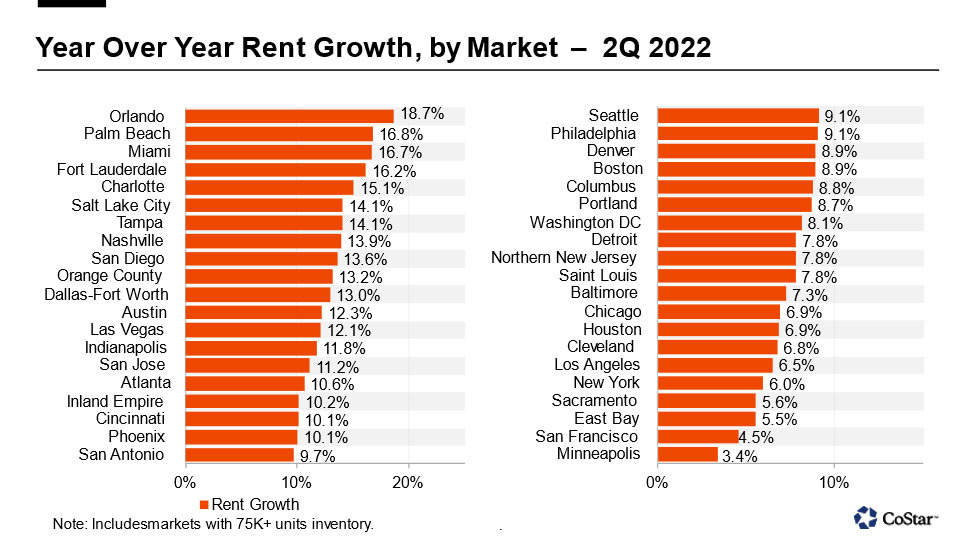

Multi-family market

Rent growth has exceeded normalized levels, with move-in rents experiencing 10-14% increases and renewals at high single digits, resulting in a blended growth rate of 10-12%.

However, this rate is not sustainable and has been driven by tight occupancy of 95-96%, aided by eviction moratoriums and student loan repayment suspensions.

Nevertheless, impending challenges are evident. A backlog of a million units awaits completion, and the ability to work remotely reduces the urgency for rental housing.

Supply increases and higher debt costs for developers have led to reduced growth expectations and potential distress for heavily leveraged operators.

Zelman predicts the normalization of blended rent growth to low single digits, precipitating capital redeployment decisions by investors.

The future of the landscape relies on capital strength and market exposure, with well-capitalized players likely to weather the storm, while markets with a significant backlog face greater pressure.

As Zelman's proprietary data suggests stabilization, lagging government figures will eventually reflect the trend, contributing to decreased inflation, particularly concerning shelter costs.

Multifamily isn't the primary concern in the commercial real estate (CRE) landscape. The real issue lies in the considerable capital flowing into the single-family rental (SFR) sector, with a significant pipeline of build-for-rent projects.

This influx has led to a decrease in investor interest, resulting in a more cautious approach toward SFR development and acquisitions for portfolio expansion.

Population: the underlying driver for future housing

The population is influenced by three key factors: birth, death, and immigration. Unfortunately, all three are currently moving in unfavorable directions.

Population growth in 2020 was at its lowest in decades, with a declining number of women in the prime childbearing age having children, a growing death rate due to an aging population, and decreasing immigration.

The perception is that there's a severe undersupply of housing, yet the issue is tied to asset pricing. Secularly, the trend indicates a reduced need for housing due to a declining population, potentially leading to more multi-generational living and household consolidation.

To the best of my knowledge, China and Japan are experiencing similar trends.

COVID

The housing market unexpectedly emerged as a pandemic winner due to consumers' preference for space and distancing.

Initially, builders ramped up land acquisition and speculative building (i.e., building without a specific buyer or contract in place for the property).

However, in 2022, a slowdown occurred as builders walked away from option agreements due to diminished demand.

However, the market has now re-accelerated, driven by resurging demand and capitalizing on the shortage in the existing home market.

Builders base their land-speculation decisions on recent sales trends. If sales remain strong, they continue to build speculative homes, as buyers prefer move-in-ready options. This contrasts with the approach of finding buyers before constructing, highlighting the market's duality.

While there's currently a cyclically driven shortage, the long-term challenge stems from population decline risks and overbuilding.

Nevertheless, public builder earnings calls indicate a renewed emphasis on speculative building (some are 60/40 spec/built-to-order, some are 100% spec), with a flexible approach to adjust based on market dynamics.

However, contemporary challenges aren't just about NIMBYs opposing growth; municipalities now struggle to provide necessary infrastructure such as sewage, water, and school systems.

Housing-related stocks

Zelman's citations really depend on market mix, not being as uniform as the new home builders.

Historically, home improvement spending averaged 4-6%, yet it spiked to over 10% across certain categories; it is now normalizing.

High-end and big-ticket segments fare better than lower-end ones, which is evident in the slowing comparisons at HD and LOW compared to the more resilient DIY sector.

Excess inventory remains as customers over-ordered, impacting new orders due to normalization.

Despite homeowner equity, lower confidence curbs aggressive spending on home improvement, in contrast to previous downturns.

The surge in pandemic-induced home improvement has pulled forward the demand and has now receded, diminishing the priority of home investments.

Environmental issues

State Farm's departure from California and Farmer's decision to not renew 100,000 policies in Florida highlight the exposure of these geographic areas to natural catastrophes.

These insurers are exiting due to financial losses, as their regulated premiums fail to account for the evolving risk posed by factors such as high temperatures, flooding, fires, hurricanes, and more.

Zelman is optimistic about the central part of the country, but I, for one, have no imminent consideration to relocate to the Midwest.

Legislations could unlock supply

Over 33 million homes are owned by investors who rent them out. Institutional investors comprise less than 2% of this segment, with the majority being mom-and-pop individual investors.

Government incentives, such as eliminating capital gains taxes upon sale to first-time buyers, could encourage selling and expanding housing inventory.

Nonetheless, job security and consumer confidence remain influential and must both weaken to drive downward pressure on home prices.

Valuation of homebuilding companies

Homebuilding companies are often evaluated on the price-to-book ratio (P/B) due to the significance of land ownership as an investment.

The key factor is the anticipated returns on these land holdings. The current median price-to-book ratio stands at 1.7x, which likely incorporates quite high expectations.

A challenge arises as land acquisition becomes difficult and inflation leads to higher land prices. Historically, valuations have normalized around 1.25-1.30x book value.

Thanks for reading. I will talk to you next time.

If you want to advertise on my newsletter, contact me 👇

Resources for your public equity job search:

Research process and financial modeling (10% off using my code in link)

Check out my other published articles and resources:

📇 Connect with me: Instagram | Twitter | YouTube | LinkedIn

If you enjoyed this article, please subscribe and share it with your friends/colleagues. Sharing is what helps us grow! Thank you.

My discussion is based on a video podcast with Ivy Zelman. If you're interested, watch the full recording below: